- Dermatology

- Surgical Dermatology

- Aesthetics

- Wellness

Patient Resources

Insurance & Self-Pay Options

At Integrative Dermatology, we understand that finances shouldn’t stand in the way of your skincare goals. That’s why we offer a variety of flexible payment options to fit your individual needs.

Insurance billing and flexible payment options

At Integrative Dermatology, we understand that finances shouldn’t stand in the way of your skincare goals. That’s why we offer a variety of flexible payment options to fit your individual needs:

Medical billing & claim processing is a complex subject. It may cause frustration and financial hardships when not considered before seeking care. When you add in variable self pay pricing and clinic policies for cosmetic procedures, it can feel overwhelming. We will break down everything for you on this page.

Note: we are not contracted with Kaiser or State Insurance.

Integrative Dermatology Payment Options

With a blend of medical expertise and advanced skincare technology, we offer tailored treatments that address both facial and body concerns.

Bill

Insurance

Patient Choice

-

Pay copay at check-in & bill 1-3 months after visit

-

Pros

-

Might be less or even $0 out of pocket

-

Out of pocket costs go towards deductible

-

Cons

-

Cannot change after claim has been submitted

-

Might be more expensive

-

Patient bills will come months after care

-

Important

-

Pathology and Lab bills are billed separately (not by Integrative Dermatology)

Self pay

Patient Choice

-

Pay at check-out

-

Pros

-

Designed for uninsured

-

Might be less out of pocket

-

Transparent pricing – no hidden costs or suprise bills

-

Cons

-

Out of pocket costs DON’T go towards deductible

-

Labs must be obtained elsewhere

-

Important

-

Pathology and Lab bills are billed separately (not by Integrative Dermatology)

Cosmetic

Self pay

Cosmetic

-

Pay at check-out

-

Pros

-

Transparent Pricing

-

Ability to seek reimbursement

-

Cons

-

Cannot be billed through insurance

-

Important

-

All cosmetic procedures are self-pay at the time of service.

Insurance Billing: How it Works

1) Patient provides insurance information

You provide your insurance information to one of our team members. This will have all the information to bill you correctly. We will do an eligibility check at or before check-in to verify your insurance is “active”.

Expert Advice:

There are dozens of “sub-plans” under every insurance plan. We do our best to know which ones we are specifically contracted with, but insurance companies are always updating and changing them often without our knowledge. It is always worth checking with your insurance company BEFORE your visit to verify if we are an “in network or “out of network” provider.

2) Patient pays “copay” at check-in

When you check in you will likely pay a “copay”. This is a partial payment made before a medical visit. Your insurance card will have a specific copay. Dermatology is usually considered a “specialty copay”.

Expert Advice:

Expect to pay more than just your copay. 75% of patients will have out-of-pocket costs beyond a copay. Patients who only pay a copay are known to have “really good insurance”. Unfortunately, we are not made privy to the intimate details of your chosen insurance. There is a lot of variation within a chosen plan and therefore it is ultimately the responsibility of you, as the patient, to know both the name of the health insurance company and plan that you have chosen, as well as what your coverage entails. Knowing whether you have a deductible (an amount you must pay before your insurance will participate) and knowing the amount of said deductible is your responsibility as the patient. We would love to know that for you, but it is unfortunately not feasible.

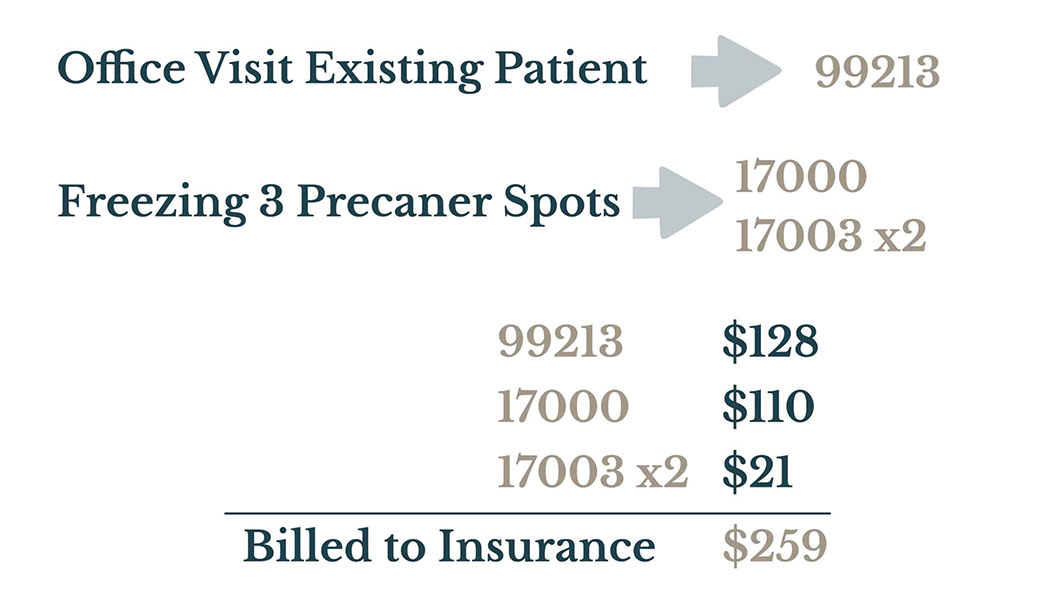

3) Diagnoses, visit, & treatments are translated into insurance codes

Procedure and visit codes called CPT codes are created based on what the doctor did. These CPT codes are paired with ICD 10 codes. Together they tell a story. The doctor did [cpt] for the treatment of [ICD 10]

Expert Advice:

Screening visits, such as skin cancer screenings, do not have planned CPT codes beforehand. More findings, more procedures, and more concerns mean more CPT codes. Planned procedures like surgeries have CPT codes predetermined. Knowing this can help you anticipate what is coming.

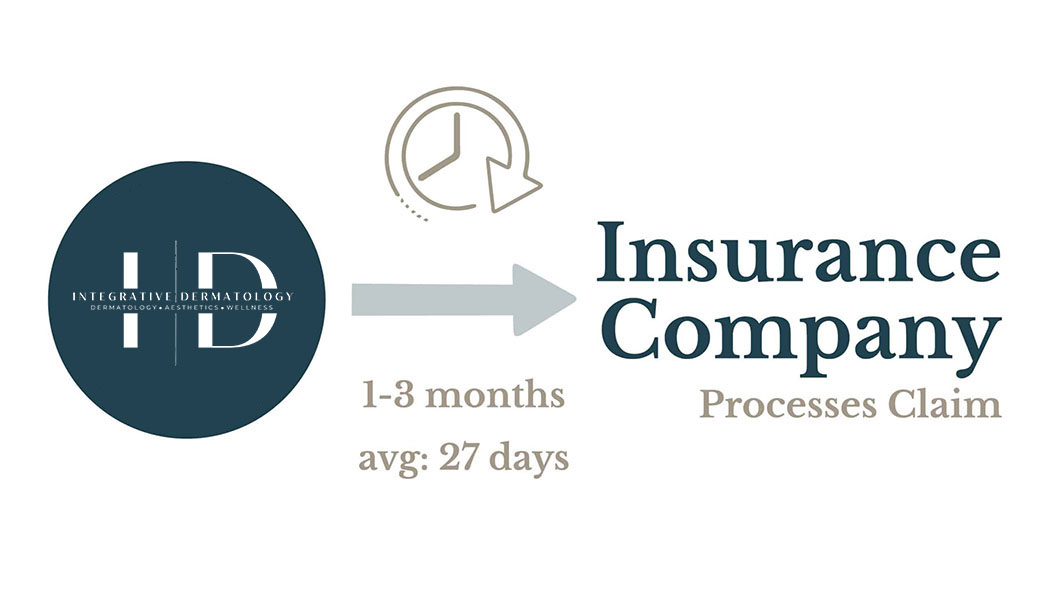

4) Codes are sent to insurance

Codes are sent through a clearing house to your insurance. The clearing house we use is Trizetto. A medical practice must send codes before a deadline called “timely filing” to ensure a visit is processed.

Expert Advice:

Our medical billing is very efficient. Our DSO is an average of 27 days. This means that we can expect to hear back from insurance 27 days from the visit. Sometimes this can take 2-3+ months.

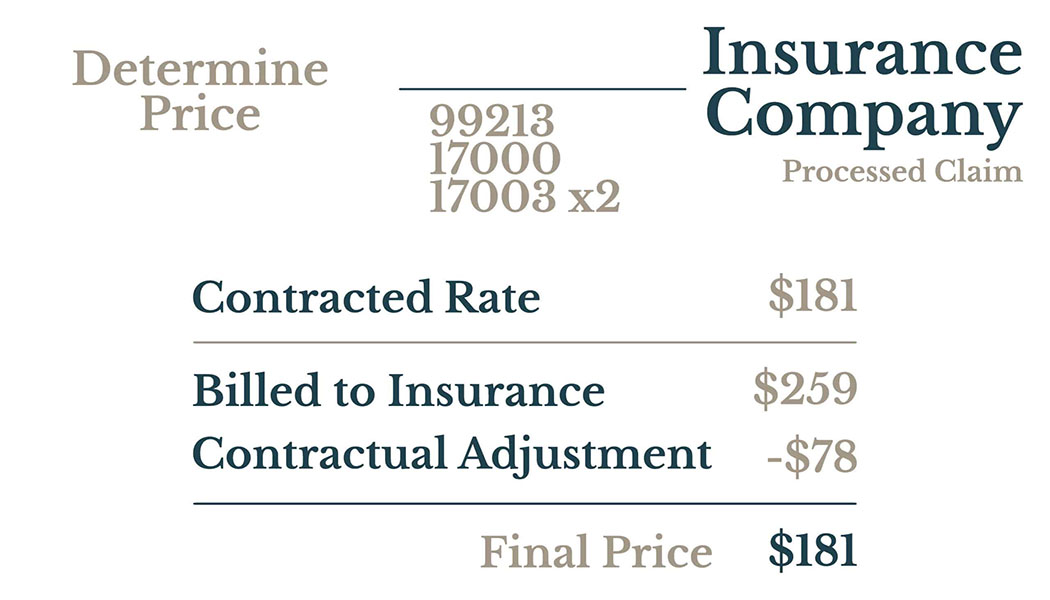

5) Insurance decide price

Codes will go through a “contractual adjustment” to determine the overall price. This is set by your insurance.

Expert Advice:

The choice to pay our “in office, same day cash price” is yours to make at the time of your visit . Once you have chosen to have your visit billed through your insurance it is sadly out of our hands as far as pricing is concerned. Your insurance company ultimately determines the cost of your visit at that point and we cannot change it. Our role is to enter into our medical software what was done at your visit and the insurance company takes over from there.

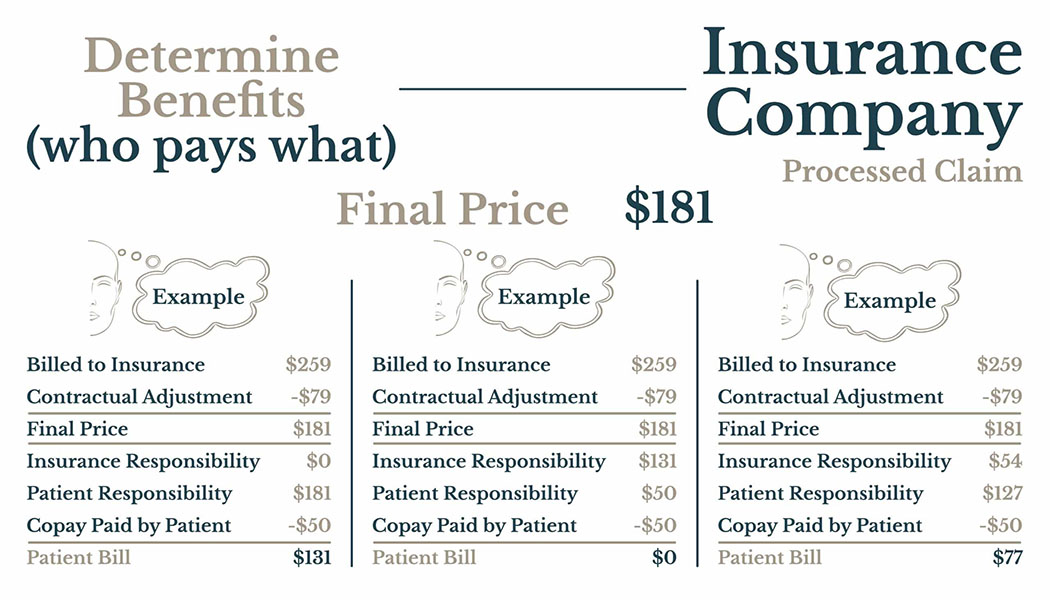

6) Insurance decide cost to you

The insurance company will decide how much they are going to pay to towards your visit. They base this on your insurance benefits. They will then decide how much you must pay.

Expert Advice:

The choice to pay our “in office, same day cash price” is yours to make at the time of your visit . Once you have chosen to have your visit billed through your insurance it is sadly out of our hands as far as pricing is concerned. Your insurance company ultimately determines the cost of your visit at that point and we cannot change it. Our role is to enter into our medical software what was done at your visit and the insurance company takes over from there.

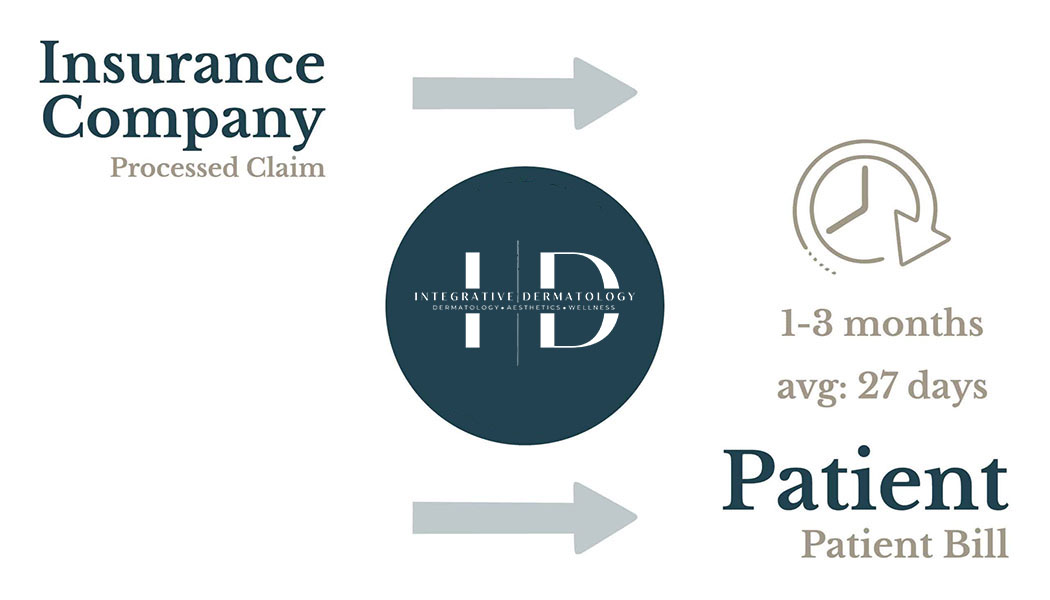

7) You will receive a bill from us

The insurance company electronically transfers their decision to us on a receipt called an EOB. This tells us exactly how much to bill you.

Expert Advice:

We want to save you money. Our cash price is typically cheaper than the cost of having “bad” insurance. We have to bill you what your insurance dictates. Changing and lowering bills from patient to patient is insurance fraud, so what your insurance says goes.

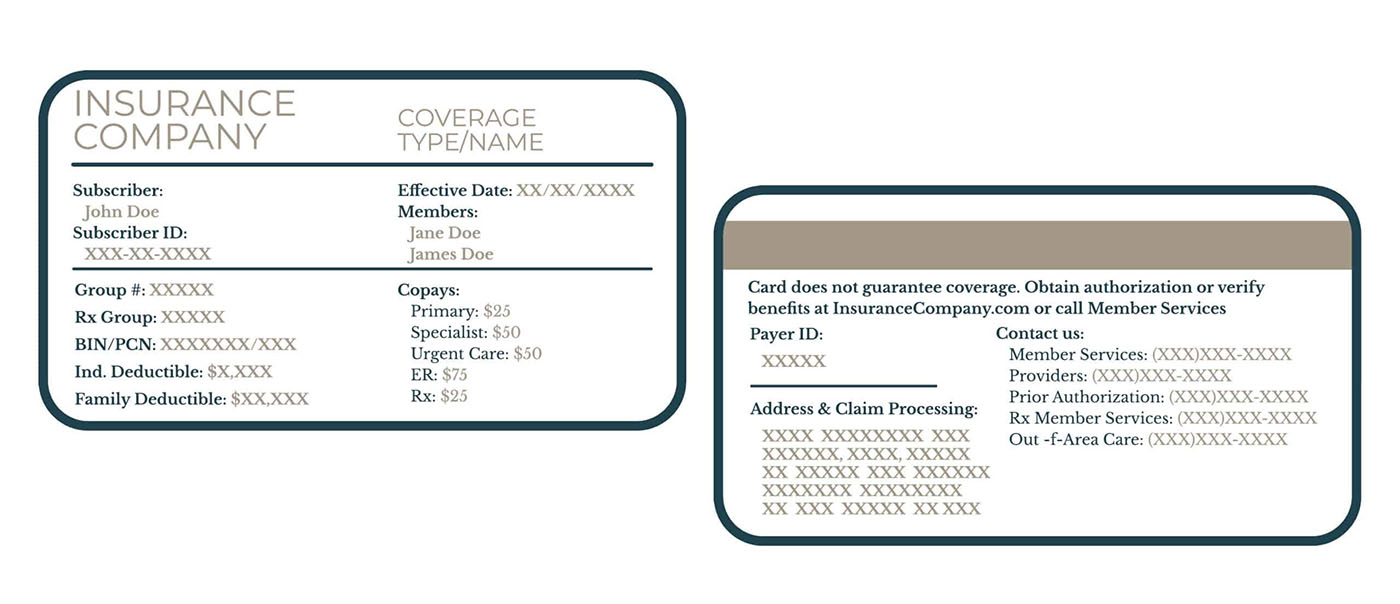

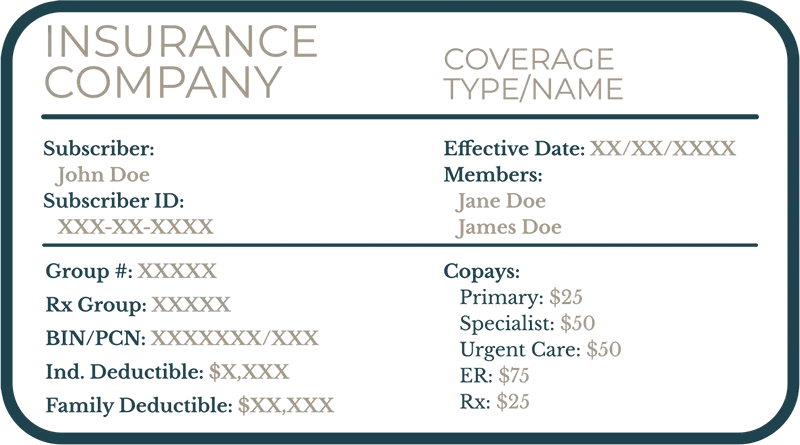

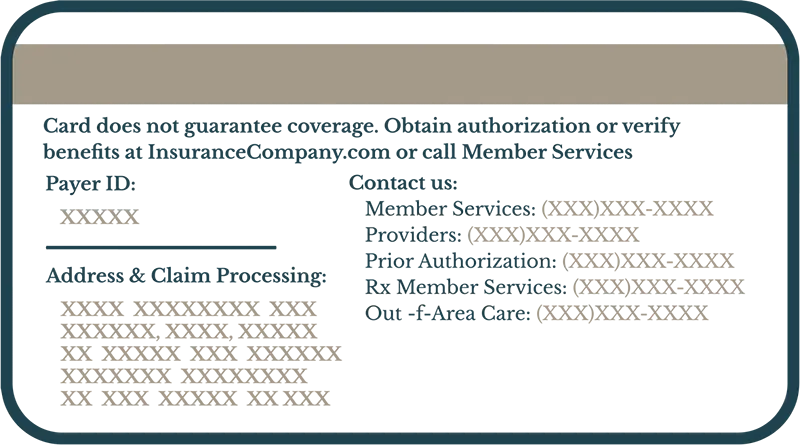

Insurance Card

How to Read Insurance Card

Subscriber

This is the name of the primary insurance holder. It’s often the person whose name the insurance policy is under (e.g., the employee, parent, or spouse).

Subscriber ID

This is a unique identification number assigned to the primary insurance holder. It’s like your personal account number with the insurance company and is essential for claims processing.

Effective Date

This date indicates when your insurance coverage began. Services received before this date may not be covered.

Members

This section lists all individuals covered under the insurance plan (e.g., spouse, children). Sometimes, instead of listing all members, it may say “See member ID card” or similar.

Group #

This number identifies the employer or group that sponsors the insurance plan (if applicable). It connects you to a specific plan offered through a company or organization.

RX Group

If your plan includes prescription drug coverage, this number may be specific to that benefit and is used when filling prescriptions.

Individual Deductible

This is the amount you must pay out-of-pocket for covered healthcare services before your insurance starts to pay a significant portion. This applies to each individual covered under the plan.

Family Deductible

Similar to the individual deductible, but this is the total amount the entire family must pay for covered healthcare services before the insurance starts to pay a significant portion. Often, the family deductible is a multiple of the individual deductible.

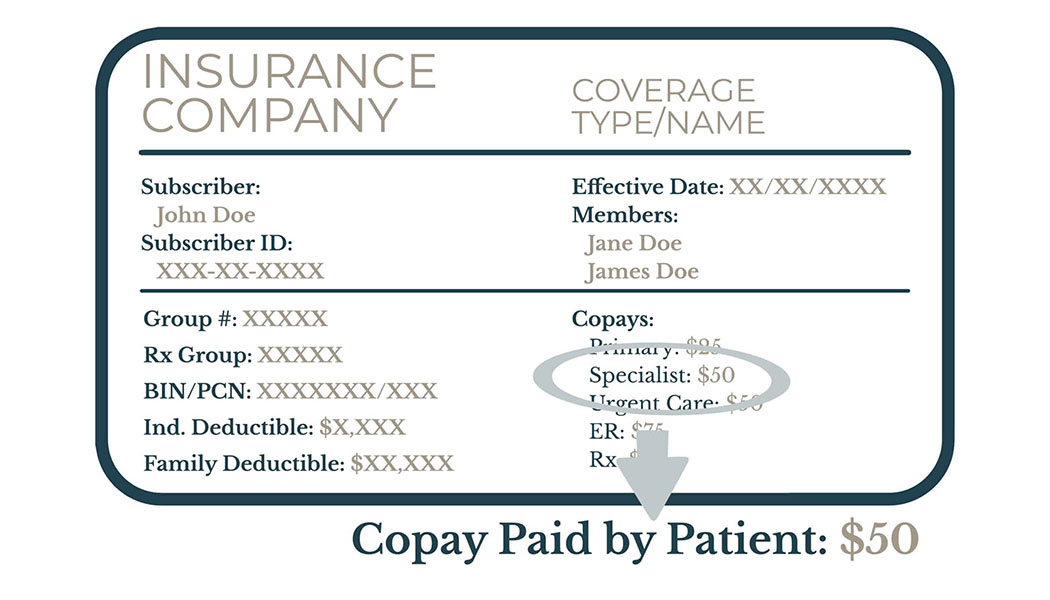

Copays

These are fixed amounts you pay for specific healthcare services, such as doctor’s visits or prescriptions. They are typically paid at the time of service. Your card may list different copay amounts for different types of services (e.g., primary care physician, specialist, emergency room).

Payer ID

This is a unique identification number assigned to each insurance company or payer. It’s used electronically to route claims to the correct insurance company for processing.

Contact Service Numbers

Your insurance card should list phone numbers for various services, such as:

- Customer/Member Service: For general questions about your coverage, claims, or benefits.

- Claims: To inquire about the status of a claim.

- Pre-authorization: To obtain approval for certain procedures or treatments.

- Nurse Line: For health advice or to speak with a registered nurse.

BIN/PCN:

These are numbers used by pharmacies to process prescription claims.

- BIN (Bank Identification Number): Directs the claim to the correct insurance company.

- PCN (Processor Control Number): Identifies the specific plan or group for prescription benefits.